The buzz is continuing to grow across the business world for Blockchain, and we have written about it in the past, but how can accountants use Blockchain to streamline their work?

Wait, how does Blockchain work again?

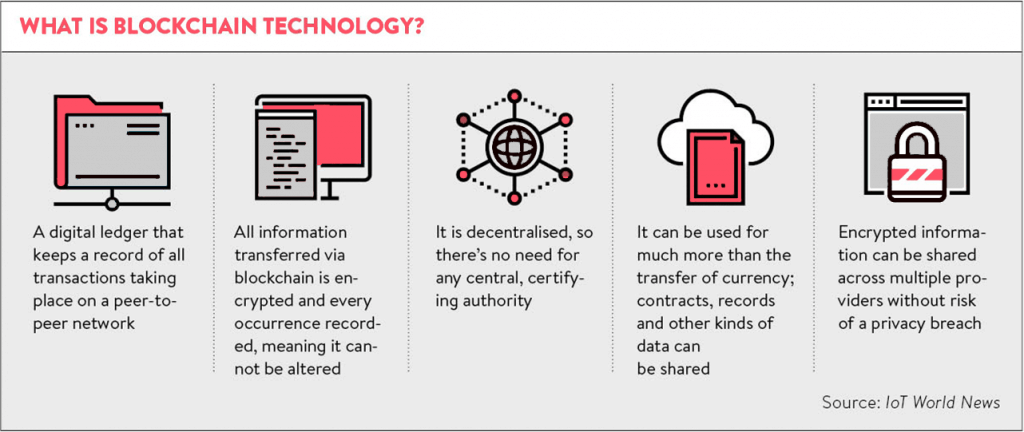

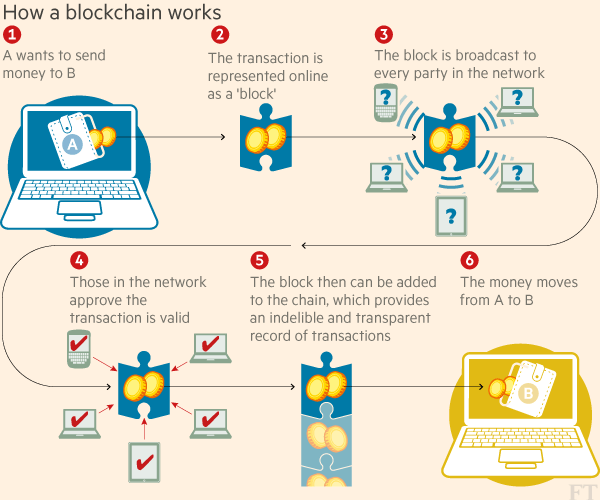

Put simply, Blockchain removes the need for storing your own transaction records through creating an audit trail on “blocks”. These blocks are public and can be accessed/maintained by all parties involved in a transaction. The audit trail of a transaction builds as more information is added, blocks are encrypted to ensure privacy breaches don’t occur. Once a block is verified and added to the Blockchain. These can’t be manipulated by others but can be corrected by those involved.

Isn’t Blockchain only useful for cryptocurrency?

Cryptocurrency brought this technology into the zeitgeist, but these applications are just breadcrumbs of what Blockchain is capable of. The motivation for the use of this technology is secure and easy exchange of information between parties. These are very important capabilities when exchanging Cryptocurrency, but also useful for accounting and bookkeeping.

Why should I care about Blockchain?

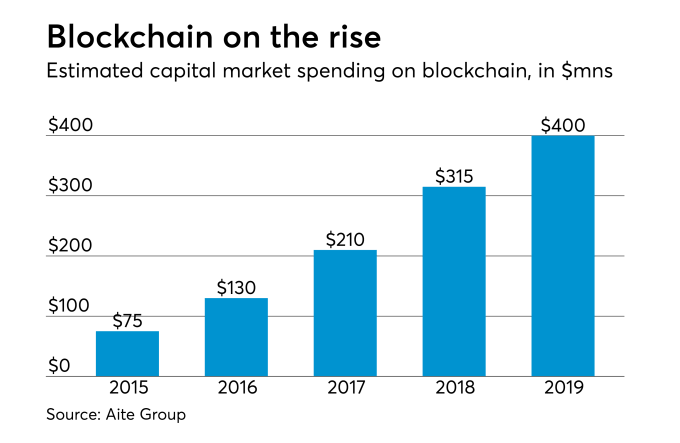

Reports from the World Economic Forum suggest 10% of global GDP will be stored on this technology by 2025. Universities are offering courses in Blockchain, the next generation of accountants will be masters before they even enter the workforce. To put it simply, Blockchain is here to stay and is growing in importance.

How is this going to change accounting?

Because transaction information is entered into “blocks” and securely stored, there is no need for parties to keep their own records of transactions. However, there may become a triple-entry system, where transactions would be entered into both the Blockchain and each party’s ledgers.

Blockchain eliminates the need for auditors to verify transactions, this means accountants will no longer have to reconcile and process transactions as parties can record and share information independently. Standardisation also allows auditors to verify large portions of data automatically, saving time and costs for audits. This marks a shift in the workflow of accountants, through shortening the process of verifying information, this opens up other opportunities.

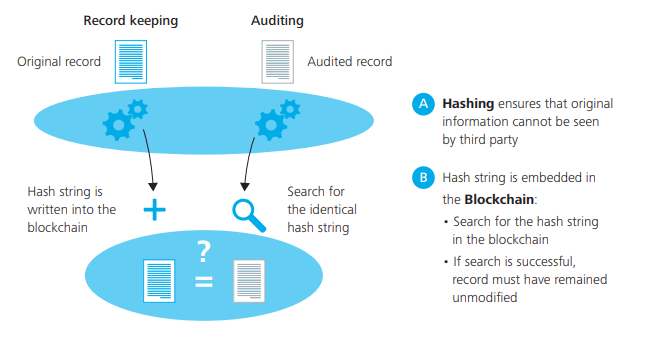

This technology can be used to improve the integrity of electronic files easily through generating a hash string of a file. Hash strings are electronic fingerprints of files which can be compared once timestamped into a file.

What changes are we seeing right now?

Robert Massey discussed the boom of Cryptocurrency business for accountants at the Accounting and Finance Show. As governments around the world develop better tax guidelines and recognition for Cryptocurrency, tax professionals will see more business.

Massey also discussed the idea of ‘smart contracts’ using Blockchain to embed contract details into third-party sources. For example, a contract where an invoice will pay for itself after checking delivered goods are received based on specifications and presence of funds in a company’s account. At the moment, ‘smart contract’ technology is being used in the legal industry, but the applications are wide spreading.

There is a lot of business in Blockchain, start to develop your knowledge now so you don’t get left behind